Award-winning PDF software

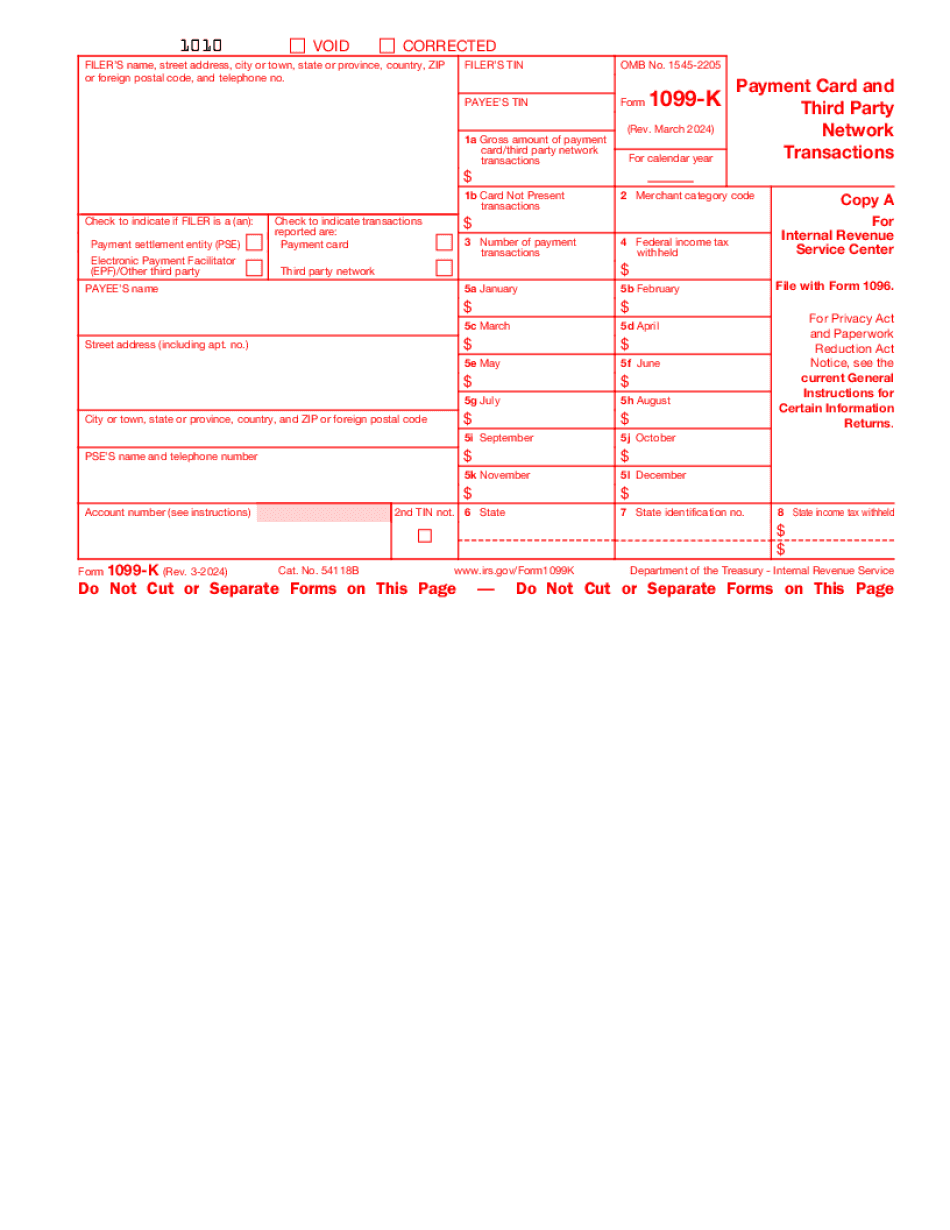

Paypal 1099-k threshold Form: What You Should Know

PayPal Payments and/or Venmo Payment If this was “still a myth”, why haven't we just moved all our payments over to PayPal? “I can't hear you. PayPal is my favorite payment app.” — A new law came into effect July 1, 2022. No more 200 PayPal deductions! Instead, we now have to report and pay in your own currency as follows: PayPal's Tax Guide for Sellers (also available in Spanish) (also available in Spanish) PayPal's Payments and Venmo Policies for Sellers (also available in Spanish) 1099-K: What You Need to Know — The Turncoat Blog Jan 9, 2025 — In September 2017, the IRS issued final rules (PDF) for collecting PayPal payments and withholding tax on them. To help out, Turncoat created a FAQ Q3 I will pay with PayPal, but don't have a PayPal account. Will I pay with a PayPal account if I owe money? A3 To be treated as a payee for a PayPal payment, a seller must have a PayPal account with the seller, and the seller must have made those payments. The seller must identify the payee on the payment. For example, if you paid for your shoes with PayPal then the bank told you that you owed 5,000 for the shoes, but you didn't have a PayPal account, you would not owe any U.S. taxes. You might want to ask the bank for a copy of the transaction to help verify that you should have been on the bank's radar. Q4 What do I do if my taxes get back to me? Can I still claim the tax deduction? A4 The answer is “Yes” the IRS will pay for your tax if the money will not affect your taxes more than 20. If the money you receive from PayPal for payment of taxes exceeds 20 it will be treated as your taxes and paid to the IRS. The IRS can make payments via Direct Deposit. The payment to the IRS will be made electronically to a U.S. bank account. A bank account is NOT required but would be helpful! We'll be posting instructions to help merchants pay your taxes as soon as the IRS issues the regulations (which could be as soon as this spring).

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 1099-K, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 1099-K online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 1099-K by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 1099-K from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.